I was recently invited to participate in a virtual seminar, ‘Building a market for exchange traded derivatives for recyclables’ (29 July 2020). That’s a fine idea, a financial market inspired solution to many practical problems facing global recycling. The recycling market is dogged by informational problems, with oversupply in some areas and undersupply in the areas where there is meaningful demand. It is dysfunctional, in the words of Rowan University’s Professor Jordan Howell, who organised the seminar. Finance theory tells us that a derivative market might be the answer, offering producers and buyers the possibility to gain some surety as to future prices and plan accordingly. Howell’s colleagues Professors Jordan Moore and Daniel Folkinshteyn shared research showing that derivatives markets tend to improve trading conditions in the underlying commodity market as well. Industry experts shared their stories about starting financial markets and managing risk through derivatives while the audience comprised industry representatives, regulators, and academics from across the United States. I was honoured to speak alongside Commissioner Rostin Behnam of the US Commodity Futures Trading Commission, who set a regulatory vision of innovative markets serving the economy through a robust and fair process of price discovery.

The event was organized by Professor Howell and his colleagues, academics from the Rowan University School of Business in New Jersey, and sponsored by the New Jersey Recycling Enhancement Act Grant Program and the Rowan Centre for Responsible Leadership. Despite the usual technological gremlins, it was a fascinating session.

My talk was titled ‘What makes a market? Understanding the social connections that underpin markets’. I was delighted to be able to say that that many of the findings of my research had already been echoed by earlier speakers, especially Stein Ole Larsen, a Norwegian entrepreneur who has founded NOREXECO, an exchange for pulp and paper.

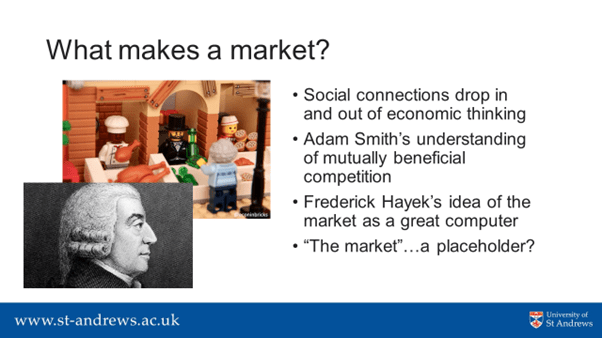

I began by remarking that we had already witnessed two distinct strands of thinking in the seminar. On the one hand, an economic account of the purpose and function of derivatives, shorn of any kind of social relationship. On the other, an account of the struggles of making such a thing happen in practice, dependent upon the complex understandings of practitioners, with vested interests, institutional constraints and ingrained habits. This reflects in many ways a broader pattern where the social drops in and out of market thinking. We have, in 18th-century notions about markets Adam Smith’s understanding of mutually beneficial competition between the butcher, brewer and baker. But by the twentieth century we see the social slipping away in economic thinking. There’s Frederick Hayek’s idea of the market as a great computer at the centre of self organising economic processes. From Hayek’s metaphors I think of some kind of steam punk machine, with entrepreneurs grappling to change the dials of this great engine of price discovery. By the time of the efficient market hypothesis the social has vanished entirely, replaced by a market full of individual atomised practitioners. But we know that markets have places and relationships: we know this intuitively from our own experiences in the yard sale or the supermarket.

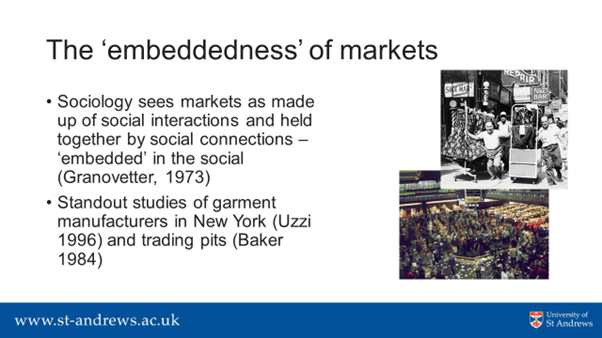

Sociology, on the other hand, sees markets as made up of social interactions and held together by social connections, embedded in the social to use Mark Granovetter’s well-worn term. A couple of classic studies will illustrate this point and we can see them in these pictures of the New York garment district and the trading pits of Chicago. There’s Brian Uzzi’s study of New York fashion manufacturers in the eighties, extending credit and support, helping competitors through difficult times; and Wayne Baker’s study of the trading pits as policed by social norms. The fundamental insight is that markets cannot function without trust between participants and market actors will tolerate less competitive prices in return for the security that comes from interpersonal relationships. In other words, market participants don’t necessarily act as economic theory suggests.

But these are old photographs. That kind of trading doesn’t exist any more. Contemporary markets are made of wires, screens, data flows algorithms, telephones (perhaps), intercoms; trading rooms and traders; traders plugged into spreadsheets and computer terminals, all supported by vast backrooms of settlement and surveillance. In fact, there often aren’t humans at all: 90 % of equities trading globally is now conducted algorithmically.

Well, research suggests that bodies still matter. The traders studies by Knorr Cetina and Bruegger strap themselves into their chair, figuratively speaking, and are immersed into the market as it through the screens. The market rolls out like a tapestry of information, circling the world with the sun. As technological advances have reshaped markets, so social connections have been worked into the technology. Knorr Cetina calls these global microstructures: tight communities dispersed globally and held together by technology, numbers on the screen, voices on an intercom. My own work has shown how the norms of trading are worked into the material devices of trade, reproducing social mores. One might even argue that algorithms capture something of their makers, although here I am at the limit of my expertise. There is even evidence to show that, in the absence of bodies, traders bind numbers back into stories and commentaries about people; I’ve watched traders at work offering a dense narrative of who is doing what is behind the stream of supposedly anonymous numbers.

But I wanted to stress that there is more to markets than trading. Markets can be understood as fundamentally social projects: they have histories, they have path dependencies, they are embedded in particular spaces and social communities; they have political entanglements from the outset. It’s easiest to show this with examples.

The picture at the left of the slide shows a crowd of stockjobbers gathering at Jonathan’s coffee house in Exchange Alley. What did they trade? The stock in the new joint-stock corporations, such as the Bank of England, all the infamous South sea company, the East India company and even the Royal Africa company. These corporations were engines of colonial exploitation but they also provided a link between the fat pockets of the merchants and the needy coffers of the nation: they lent vast sums to the government which were pushed through their balance sheets and parcelled out as tradable stock. Eventually the richer brokers bought a building on Threadneedle Street and began to charge rent. Here we have demonstration of classic social theory, which shows that market participants exploit status relationships in markets to maintain their position. Until 1986 this pattern of trading persisted, with jobbers trading face-to-face on the floor of the exchange.

Then we see a picture of the nineteenth century building of the Chicago Board of trade. I talked about the evolution of Chicago’s Board of Trade as an association of politicians and businessmen to help the city as well as build a market and a series of buildings that grew to house evolving trading practices. Professor Moore had previously given us a financial perspective on derivatives, alienated from their place in history. The Chicago story gives them a history and social context, first of all with the development of ‘to arrive’ contracts, the beauty of which was that they never had to arrive, and then crowned by the legalisation of derivative trading in the United States. This came out of a legal battle between bucket shop magnate CC Christie and the Board of Trade, and ended with Justice Holmes of the Supreme Court ruling that speculation ‘by competent men is the self-adjustment of society to the probable’. Speculation, as colleagues had made clear earlier in the session is not necessarily a bad thing.

It’s important to add that social connections can cause problems too. Here’s a few examples to make that point. Innovation coupled with social prestige not always a good thing…Think of the project to legalise mortgage bonds under Louis Ranieri at Salomon Brothers in the 1980s, which contributed to the boom and bust of that decade, or the JPMorgan diaspora around collateralised debt obligations in the late nineties. Put the two together and you end up with a calamity on the scale of the 2008 credit crisis.

At the other end of the scale, my own work has shown how Taiwanese retail investors take up the occupation as a means of entry to status groups. So social networks can be cliques, and worse. Donald MacKenzie suggests that dense social networks among hedge fund managers in the late 1990s led to the bust following the collapse of Long Term Capital Management. The hedge fund managers, members of a geographically and socially close community, knew where the smart money was and followed it. The result was a super portfolio that greatly amplified the consequences of Russia’s default on the ruble in 1998. In contemporary times, Karen Ho’s superb ethnography of Wall Street recruitment among elite shows how social connections reproduce particular kinds of gender, race, and class differences.

For this reason, regulation seeks to drive the social out of markets. We are all familiar with the dominant conception of efficient markets, associated with Eugene Fama. Here informational efficiency equals allocative efficiency (under Walrasian assumptions, to be technical). What is needed is a crowd of anonymous buyers meeting a crowd of anonymous sellers, all transactions listed in the broad daylight of the exchange’s order book, and these arrangements are built into the architecture of mainboard equity markets worldwide.

But there’s plenty of evidence that social connections are vital for market operation. There are organisational reasons such as training the next generation of market practitioners and maintaining appropriate cultures. Scholars have shown that social interactions are a major source of innovation and profitable trading strategies – though the credit crisis reminds us that innovation is not in and of itself a good thing.

More important is the relationship between social connections and resilience. March 2020 saw the third major crash since the digitization of markets in the 1980s. Such was the severity of the collapse that automated fail-safe devices struggled to keep up with the speed of market falls. This kind of collapse is the result of the removal of the social. Even in benign times, HFT remains notoriously unstable and presents new challenges to regulators. The ‘Flash Crash’ of 6 May 2010 remains the paradigmatic instance of algorithmic instability but it is far from the only such event.

Meanwhile studies offer glimpses of resilience based on social connections. Daniel Beunza showed how what he called heterarchical (the opposite of hierarchical) organisation helped trading firm cope in the days following 9/11. Donald MacKenzie records how, in the aftermath of black Monday 1987, the Chicago mercantile exchange “and thus the entire global financial system) was saved from collapse only by personal relationship between the exchange chairman, Leo Melamed, and senior figures in the banking industry. He’s quoted as saying – and this is wonderful – ‘Wilma, you’re not going to let a stinking couple of hundred million dollars cause the Merc [Mercantile Exchange] to go down the tubes, are you?’ We heard a great deal in the seminar about how the clearing system guarantees the resilience of derivative markets; this example shows that the clearing system itself is guaranteed by social connections.

Finally, my research has shown how it is possible to regulate for social relations rather than against them. I’ve studied the setting up of the London Stock Exchange’s junior market AIM. Rather than imitating the costly and cumbersome in-house regulation of the Official List, the designers of AIM sought to utilise the reputational capital of financiers working around the market. Every company that comes to aim must be supported by a nominated adviser, or Nomad. There are rules about who can be a Nomad, largely dependent on existing experience in the market; everyone therefore knows everyone, and a Nomad who brings substandard offering to market will find themselves unable to conduct future business. Offer prices are worked out by negotiation between institutional investors and Nomads; investors satisfy themselves as to the quality of the advisor as much as they do the investment, and prices reflect the sum of available information. In other words, AIM looks more like one of those producer markets first identified by economic sociology (perhaps even by Adam Smith) where prices and qualities are set by producers who reflexively observe themselves and their competitors. Does it work? Well, aim has grown steadily over two and half decades, and crucially there hasn’t been the expected flow of companies up to the official list – moving from AIM is costly in terms of social capital.

In conclusion, I summed up the points I wanted to leave with the audience as they sought to set up this new derivatives exchange: markets are deeply embedded in the social and social connections are often viewed as problematic, but need not be so; social connections are a source of trust, of market stability and robustness, of information flow. Finally, I stressed that it is possible to regulate social connections in, not out. In a market so dependent on face-to-face, or at least phone to phone, interpersonal dealing and deeply ingrained habits as the waste and recycling industry, I wonder if this is a viable way forward.