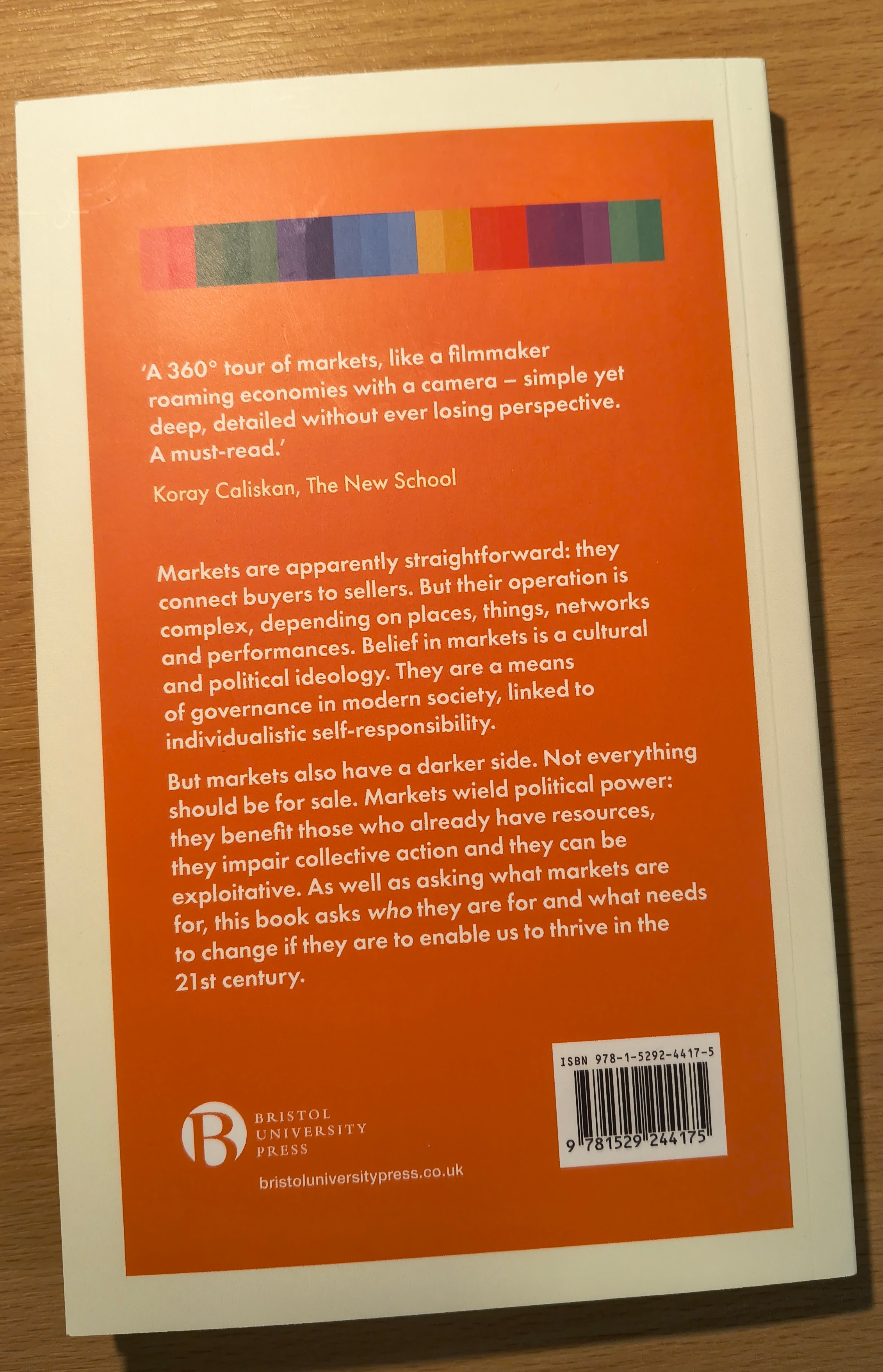

My contribution to Bristol University Press’ scorching “What is it for?” series, edited by George Miller, is in my hand and very soon in a bookshop near you.

It’s fantastic when a series title makes you think really hard about something you take for granted. I’ve been working on the sociology of markets my whole career, but still: What are markets for?

The easy answer is that they get us the things that we want and need.

It turns out, though, that markets are really for all sorts of things.

They connect buyers and sellers, of course, but depend on places, things, networks, stories, and performances. The simplest transaction in the supermarket, buying something for my supper, ties me into a global arrangement of supply chains, producers and manufacturers, banking and financial information, stories about calories and happy cows or virtuous tofu, affective relations with brands and places. All I wanted was a burger!

Markets are an ideology, a mode of governance: we all live in a market society, we need to be entrepreneurial, individual, risk takers. When SpaceX lands unbidden in our pension plan – a more likely outcome than getting to Mars – we’re owning a part of a story, a dream, a rush of techno capitalism, the spectacle and pageant of high finance. We’re also looking at an entity created by law and contract, and one that rolls out the expansionist dreams of markets into a new space. Markets have dark histories of accumulation, and we can wrangle over what should and should not be for sale.

As we look at crisis of all kinds and the end of an era, it might be that markets are partly culpable. Perhaps markets have got us too much of what we want, and now the environment is paying? Perhaps the thing that makes markets so attractive, the separation of buyer and seller, the break from endless obligations of gift, is also the root of the problem? How do accountability and responsibility cross that demarcation?

We can think about what markets might be and how we can civilise this wonderful creature that has – just maybe – got somewhat out of hand.

All that in 150 pages. Phew! And there are pictures.

What people say –

A 360° tour of markets, like a filmmaker roaming economies with a camera – simple yet deep, detailed without ever losing perspective. A must-read.’ Koray Caliskan, The New School

‘Politically engaged and engagingly written, this book equips social scientists with the necessary tools for investigating and tinkering with markets.’ Paul Langley, Durham University

‘A compelling, lucid rethinking of markets as political, moral and material arrangements shaping who prospers and who does not. A must-read for all those interested in understanding how our economy works.’ Katy Mason, University of Salford

‘What Are Markets For? is a deceptively simple question that starts to unravel as soon as you pull at the strings that make markets and hold them together. This is what Philip Roscoe does in this lively and compelling book.’ Bill Maurer, University of California, Irvine

‘This book accomplishes an almost impossible feat: sketching the contours of an extremely complex entity – the market – in a highly accessible and entertaining manner.’ Susi Geiger, University College Dublin

I’d like to thank everyone involved along the way: editor George Miller, with the sharpest of eyes and endless patience, all the production people at BUP, especially Alexandra Gregory, and the sales team too. Thanks to the readers: Katy Mason, Liz Mcfall, Paul Langley, Bill Maurer and to Teea Palo for lending me Santa (absolutely for the last time!)

Plus everyone I’ve talked to over the years, about this book, about markets.