Happy Easter everyone! Here’s a little easy listening if you’re relaxing in the sunshine. I’m delighted to be able to share this podcast, put together by Jess Miles and Bristol University Press. Jess and I chatted about the darkly comic world of finance, why it matters to us as citizens, and why we need to understand how it works. I think Jess, as a finance-studies newbie, was convinced. Thanks Jess and BUP for inviting me onto the podcast. I hope you enjoy listening.

All that money with nowhere to go: a Silicon Valley problem

I dissect Silicon Valley Bank’s utopian problem in a recent piece for the Transforming Society blog…

BBC Radio 3 Freethinking on Debt

Twas the night before Budget day and all through the house, nothing was stirring but BBC Radio 3 Freethinking and a very excellent discussion on ‘Debt, from the South Sea Bubble to Sunak’. As the nation waited for Chancellor Jeremy Hunt’s next moves on the UK’s crisis ravaged economy, Anne McElvoy hosted a high powered panel: Professor Kenneth Rogoff, Maurits C. Boas Chair of International Economics at Harvard University; Vicky Pryce, former Joint Head of the United Kingdom’s Government Economic Service, Dr Dafydd Mills Daniel, lecturer in Divinity from the University of St Andrews, and of course, your humble correspondent. It was a fun discussion – I hope you enjoy listening!

The ‘Anthropology of Entrepreneurship’ by Richard Pfeilstetter

On 2 November, I was given the opportunity to participate in a panel debate – a ‘book lunch’ (very droll!) – for anthropologist Richard Pfeilstetter’s recent (2022) book ‘The Anthropology of Entrepreneurship.’ Thank you Richard for the invitation and to Kirsty Osborne and the University of St Andrews Entrepreneurship Centre for organizing. I ended up writing a review of sorts. Richard felt it was worth sharing, so here it is (in a slightly tidier form).

“Thank you everyone for the opportunity to participate in this discussion, to Kirsty for organizing. I found Richard’s book simultaneously engaging, challenging, stimulating and at times infuriating. For an outsider to anthropology the book provided an engaging and swift tour of the strange history of entrepreneurship studies in anthropology. The source of my infuriation was simply that the tour is, for an outsider, sometimes a little too swift. Richard has managed to cram so much into a slim volume. So much, but at times, and necessarily, never quite enough.

Richard’s argument centres on a call for anthropology to take entrepreneurship seriously. He is bothered that anthropological scholarship often dismisses anthropology as a native term, something that doesn’t need to be explored reflexively, but just can be deployed in situ. Hence, he suggests, the willingness of much contemporary anthropology to regard entrepreneurship as part of a programme of social coercion and behavioural adjustment on the part of neoliberal elites.

Continue reading “The ‘Anthropology of Entrepreneurship’ by Richard Pfeilstetter”Mentioned in the New Yorker!

It’s not every day one is quoted – not just mentioned but quoted! – in a publication as eminent as The New Yorker, so you will forgive me for adding it to the scrapbook. The article, a review of Elizabeth Popp Berman’s new book ‘Thinking Like an Economist: How Efficiency Replaced Equality in US Public Policy‘ has me mentioned next to the late great David Graeber. We are the obligatory econ-hating-lefties in Idrees Kahloon’s ‘war on economics’ (see left) but still. I’m very glad to be in Graeber’s company, too.

The line itself comes from a blog I wrote for the LSE back in 2014, following the publication of my book I Spend therefore I Am (Viking, 2014, republished by Penguin as A Richer Life, 2015, and now available for less than a fiver, so knock yourself out). The book ruffled a few feathers among reviewers, just as Elizabeth Popp Berman seems to have done, and the blog was something of a reply to critics. Here it is:

Tools for thinking: a sociological take on the USS pension dispute

I teach fourth year undergraduates a module called ‘sociology of finance’. It’s a kind of mash-up of the ‘social studies of finance’, economic sociology and a little critical political economy. This semester, I had to explain to students why I was taking part in industrial action over cuts to our pension, and I tried to do using the ideas we worked with in class. If social theories are tools for thinking, as I always tell the students, we should try to use them when we can. That converstion continued on the picket line and grew into a seminar for colleagues. They liked it, and so I recorded a verson to share. The central argument is that the tools of valuation – all those ‘gilts plus’, ‘discount rates’, and ‘prudence’ – offer a space where things happen and political contestations are worked out. In every financial valuation, paraphrasing Greta Krippner, lies a history of contestation and struggle. To move towards an outcome that is satisfactory for everyone, I believe this is where we need to focus our attention; our dispute as as much about the sociology of knowledge as it is old-fashined industrial relations.

Here it is. I hope you find it helpful, informative, and not too partisan. I hope you like it too, and if you do, please pass it on.

So, I’ve finally finished that podcast…

In January 2019 I decided it might be interesting to have a go at doing a podcast. There’s something enticing about jumping into the podcast space, crowded though it might be, the thought that you can record a few words and the next thing find yourself available on iTunes, Spotify, and other such platforms. So I bought myself a microphone, read up on the necessary infrastructure, drew a logo, sketched out a plan of what I might say. I’ll have it all wrapped up by the autumn, I thought.

Everything always takes longer than you think. Nearly two years later, I have finally published the concluding episode of ‘How to build a stock exchange’. Over 18 episodes, the podcast has offered a social history of finance as we know it today, exploring the sociology and materiality of financial markets, and showing how contemporary exchanges have evolved from local concerns to global data infrastructures. The narrative features much of my original research on the markets of London throughout the twentieth century, and a smattering of anecdotes from my own youthful experience, in the days before I realised that writing about finance was far more interesting than trying to do it.

More importantly, the podcast is an attempt to find new voices for research and to disseminate more widely the intellectual concerns of a critically-inclined management scholar. In the final episode I invoke Hunter S Thompson and the spirit of gonzo: aiming for an intimate, first person take that emphasises spontaneity and raw authenticity over form and polish, where ‘deliberate derangement of the senses… de-familiarises reality, opening the door to paradoxically clearer perceptions, a twisted perspective..’ (I borrow the words of literary scholar Jason Mosser). An honest telling of our own stories, I suggest, is the best way we have of finding our moral compass in this complicated world; it certainly seems to have more integrity than writing critical articles about four-star journals in those same four-star journals. It is, says José Ossandón of Copenhagen Business School, a ‘genre-widening event’:

(as seen in ‘Lock Stock’)

So the podcast zoomed between my own research, the rich offerings of the field of the social studies of finance, and a curious selection of anecdotes from the field: breakfast with some global heavies in the Cadogan Hotel (episode 15), malicious croquet and business angels (episode 4), surfing the fringes of dotcom London (episode 13) from stuffy offices behind the sooty Victorian ironwork of the still functioning Borough Market, all rats and squashed vegetables. London in the 1990s seems a world away, containing both the promise of a unbounded global world and the seeds of the present globalised mess that we find ourselves in. Along the way it explored themes such as gender inequality in financial markets (episode 10) and the murky history of finance and slavery (episode 17). The latter topic, written in response to the Black Lives Matter movement, explored Liverpool’s burgeoning financial sector and the narrator’s own connections to the city. It led to an article in The Conversation, ‘How the shadow of slavery still hangs over global finance’. In July 2020, I was invited to address an audience of US policymakers and regulators, alongside Commissioner Rostin Benham of the US Commodity Futures Trading Commission, to discuss a possible exchange for recyclable materials, and I talk more about this possibility features in the final episode.

The podcast has been downloaded twelve and a half thousand times and the transcriptions accessed a further ten thousand times. The Guardian’s Aditya Chakrabortty described the podcast as ‘brilliant and searching’, while others said ‘beautifully told, fascinating, and very important’ (Dr Paul Segal, Kings College London), ‘an absolutely wonderful way of disseminating research’ (Dr Kristian Bondo Hansen, Copenhagen Business School), and – my favourite – ‘overwhelmed at how good this podcast is’ (Guppi Kaur Bola, activist and writer, Chair JCWI).

It’s not too late if you haven’t found it yet: the podcast is available in full from this site on the podcast page.

Write a great essay in 12 (easy!) steps!

A couple of years ago I jotted down a step-by-step guide to help my son get started on his university essays. That’s always the most difficult bit of writing – starting – and it never gets any easier. I thought some other might find it useful as well, so I’ve put it on a short video. Have fun! Beware, last minuters: the first step is ‘start early’.

I hope this helps avoid a few essay crises. If you like it, pass it on! PS: you don’t have to go to the bar in step 12 if you don’t want to.

How the shadow of slavery still hangs over global finance

[published in The Conversation, 21 August 2020]

Philip Roscoe, University of St Andrews

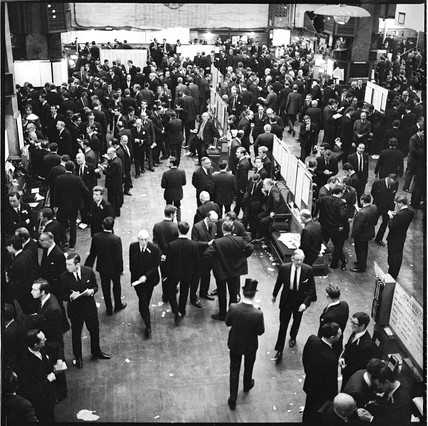

When the infamous Zong trial began in 1783, it laid bare the toxic relationship between finance and slavery. It was an unusual and distressing insurance claim – concerning a massacre of 133 captives, thrown overboard the Zong slave ship.

The slave trade pioneered a new kind of finance, secured on the bodies of the powerless. Today, the arcane products of high finance, targeting the poor and troubled as profit opportunities for the already-rich, still bear that deep unfairness.

The Gregsons, claimants in the Zong trial, were merchant princes of 18th century Liverpool, a city that had quickly grown to be one of the world’s leading commercial capitals. The grandiose Liverpool Exchange building, opened in 1754, boasted of the city’s commercial success and the source of its money, its friezes decorated with carvings of African heads.

But Liverpool’s wealth also stemmed from its innovations in finance. The great slave merchants were also bankers and insurers, pioneers in what we today call financialisation – they transformed human lives into profit-bearing opportunities.

From the point of view of merchants, the Atlantic trade was slow, unreliable and risky. Ships were threatened by disease, by poor weather, and by the constant threat of insurrection. To speed up the flow of money, merchants began to issue credit notes that could travel swiftly and safely across the ocean.

Slaves would be purchased in Britain’s African colonies and transported to the Americas where they were sold at auction. The merchant’s agent would take the money received and rather than investing it in commodities like sugar or cotton to be sent back to Liverpool, they would send a bill of exchange – a credit note for the sum plus interest – across the Atlantic.

The bill of exchange could be cashed at a discount at one of the many banking houses in the city, or replaced by another, again at a discount, to be dispatched to Africa in payment for more human chattels. Credit flowed swiftly, cleanly and profitably.

Obscenely novel

This evolution of private credit did not originate in Liverpool. It had underpinned the Florentine banking dynasties of the 15th century and gave rise to money as we know it now.

The obscene novelty of the slavers’ banking system was that this financial value was secured on human bodies. The same practices continued on the plantations, where the bodies of slaves were used as collateral on loans allowing the expansion of estates and the acquisition of yet more productive bodies. The slaves were exploited twice: their freedom and labour stolen from them, their captured “economic value” leveraged by cutting edge financial instruments.

The Liverpool merchants also pioneered the use of insurance as a means of guaranteeing the financial value of the their commodities. The slavers had long recognised that the only way to survive the occasional total losses that expeditions incurred was to gather together in syndicates and share the risk.

So when the captain of the Zong realised he was unlikely to land his cargo of sickening and malnourished slaves, he ordered 133 souls to be thrown overboard. The perverse legal logic was that if part of the cargo had to be jettisoned to save the ship, it would be covered by the insurance.

These bodies-as-financial-commodities had only speculative value. Insurance made it real and bankable. This was true in 18th century Liverpool and it remains so in 21st century Wall Street.

Financialisation today

Financialisation has since taken many forms, but basic elements remain the same. It is based on uneven power relations that capture future individual obligations and make them saleable. The contracts underlying the 2008 credit crisis, for example, turned future mortgage payments into tradeable financial securities with actual present value.

For those issuing the bonds, the profit was risk free. The risk was borne by predominantly poor Americans, whose adverse credit ratings and lack of financial skills made them easy prey for the issuers of mortgages so constructed as to lock them into economic bondage. These people were disproportionately black, Latino or migrant.

Insurance played a part here, solidifying the speculative value of investments to the benefit of traders. And when the bubble finally burst governments stepped in to maintain this system, the US Federal Reserve supporting giant insurer AIG to the tune of US$182 billion (£139 billion) while many people lost their homes.

The credit crisis bailout is eerily reminiscent of another. By the time of abolition slave ownership was so embedded in British society that the government was forced to compensate individual owners for the loss of their capital – it required an enormous loan that taxpayers only finished paying off in 2015.

I’m not saying that bankers today are like slave traders. But I am saying that contemporary finance is still riddled with regimes of dominance and exploitation at work.

Take contemporary philanthrocapitalism, where finance seeks to do good while also benefiting investors. Novel financial instruments position social problems as an opportunity for profit. The bodies of prisoners, for example, become implicated in schemes to prevent recidivism with personal character reform the trigger for investment payouts.

Schemes such as this make social problems the responsibility of individuals and ignore the structural relations of austerity that lie behind them. Finance wins twice, praised for solving the very same problems that it has benefited from creating.

Beware financiers bearing gifts. Student loans, mortgage bonds, social impact bonds, even biodiversity investing – all earning rents from the captured future activities of relatively powerless individuals – bear the shadow of the Atlantic trade.

Philip Roscoe, Reader in Management, University of St Andrews

This article is republished from The Conversation under a Creative Commons license. Read the original article.

What makes a market? Understanding the social connections that underpin markets

I was recently invited to participate in a virtual seminar, ‘Building a market for exchange traded derivatives for recyclables’ (29 July 2020). That’s a fine idea, a financial market inspired solution to many practical problems facing global recycling. The recycling market is dogged by informational problems, with oversupply in some areas and undersupply in the areas where there is meaningful demand. It is dysfunctional, in the words of Rowan University’s Professor Jordan Howell, who organised the seminar. Finance theory tells us that a derivative market might be the answer, offering producers and buyers the possibility to gain some surety as to future prices and plan accordingly. Howell’s colleagues Professors Jordan Moore and Daniel Folkinshteyn shared research showing that derivatives markets tend to improve trading conditions in the underlying commodity market as well. Industry experts shared their stories about starting financial markets and managing risk through derivatives while the audience comprised industry representatives, regulators, and academics from across the United States. I was honoured to speak alongside Commissioner Rostin Behnam of the US Commodity Futures Trading Commission, who set a regulatory vision of innovative markets serving the economy through a robust and fair process of price discovery.

The event was organized by Professor Howell and his colleagues, academics from the Rowan University School of Business in New Jersey, and sponsored by the New Jersey Recycling Enhancement Act Grant Program and the Rowan Centre for Responsible Leadership. Despite the usual technological gremlins, it was a fascinating session.

My talk was titled ‘What makes a market? Understanding the social connections that underpin markets’. I was delighted to be able to say that that many of the findings of my research had already been echoed by earlier speakers, especially Stein Ole Larsen, a Norwegian entrepreneur who has founded NOREXECO, an exchange for pulp and paper.

{kind=link}